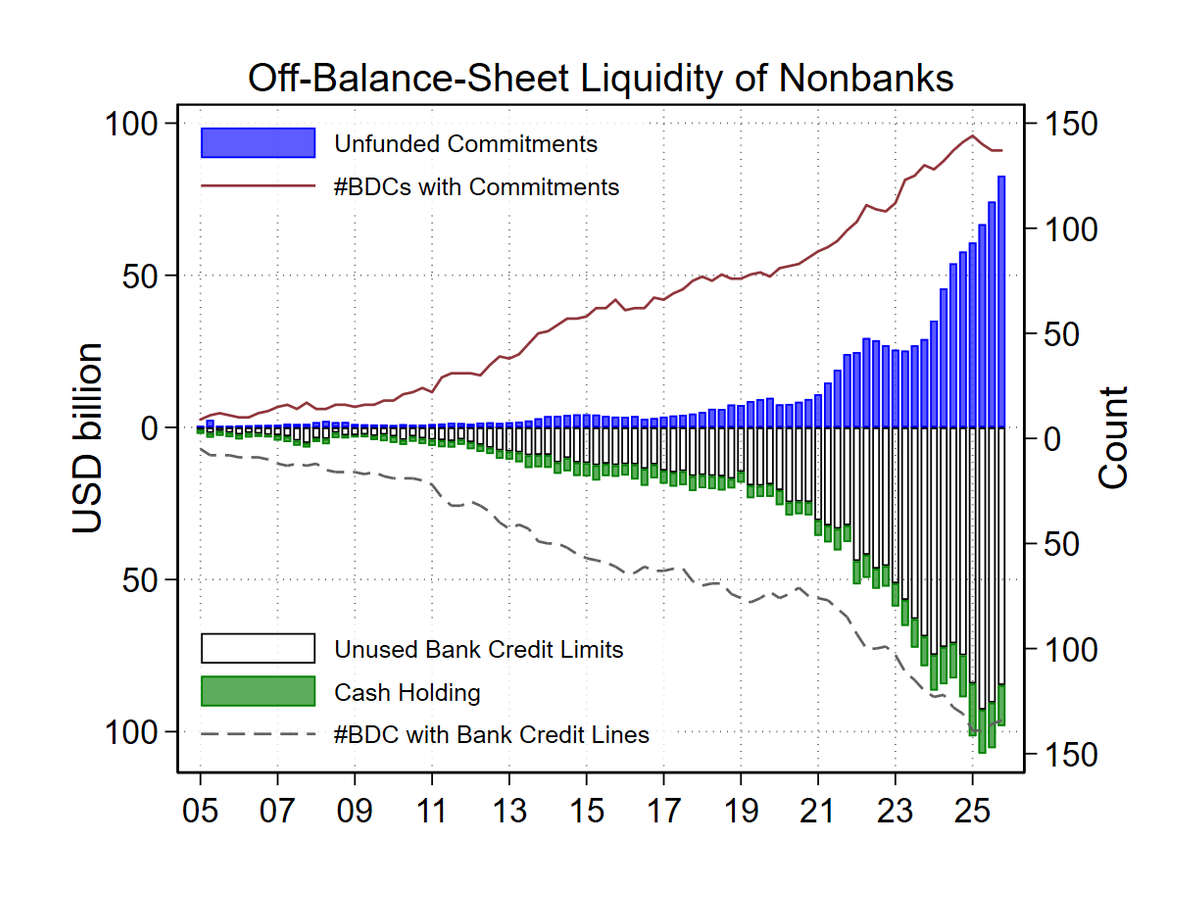

Credit Commitments by Nonbanks

Abstract

Despite the secular shift to nonbank lending, banks retain a distinctive advantage in providing credit lines (Kashyap, Rajan, and Stein, 2002). We document a new pattern in nonbank lending: business development companies (BDCs) extend substantial credit commitments to borrowers, with commitment-to-asset ratios comparable to those of banks. These off-balance-sheet commitments are concentrated, exposing BDCs to undiversified borrower liquidity shocks—a risk they manage with credit lines provided by banks. We develop a model of layered liquidity insurance along the credit chain: the BDC pools its portfolio firms to partially diversify idiosyncratic shocks and uses a bank credit line to backstop residual liquidity risk. In equilibrium, the nonbank optimally provides only partial liquidity insurance, which generates a novel externality whereby firms sharing the constrained liquidity pool inefficiently underinvest in liquidity management.